Blockchain has been presented as a breakthrough technology that has proven its potential in not just one industry but across sectors from finance, supply chain, healthcare and beyond. However, the blockchain technology has its pros and cons.

The main blockchain technology pros and cons will be covered in this article.

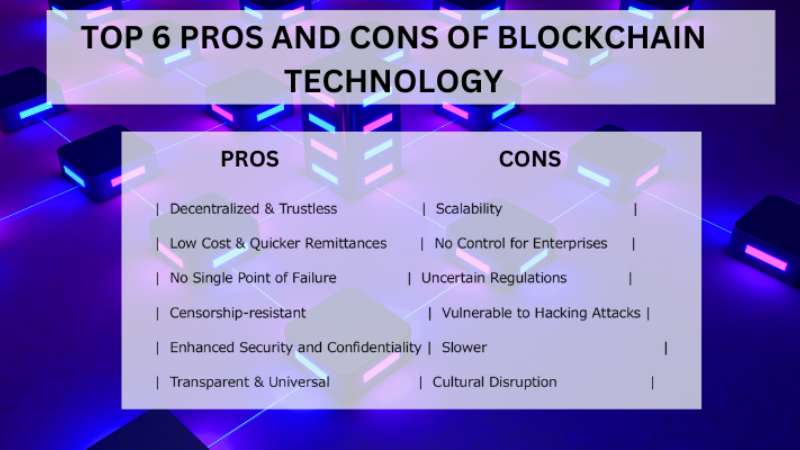

Top 6 Pros and Cons of Blockchain Technology

Blockchain technology offers numerous advantages for its potential to various industries.

However, like any technology, it also comes with its drawbacks.

Below is a list of the top 6 blockchain technology advantages and disadvantages, followed by detailed explanations.

Advantages of Blockchain Technology

Here, we look at the benefits of blockchain technology.

1. Decentralized & Trustless

The best cryptocurrencies rely on blockchain technology, which ensures decentralization and security.

A blockchain facilitates peer-to-peer value transfer without relying on intermediaries or central authorities.

Data is stored across a decentralized network of servers and validated through consensus, enabling transactions between parties who don’t need to trust each other.

One advantage is the elimination of intermediaries, which often charge fees and may lack transparency.

This removal can increase trust by reducing the potential for corruption and dishonest practices associated with intermediaries, ultimately improving the efficiency and integrity of transactions.

2. Low Cost

Blockchain removes the need for central servers, cutting costs. Transactions happen directly on the blockchain without middlemen, reducing banking and payment processing expenses.

Contracts and transactions are automated, reducing the need for humans to intervene.

As a result, end users benefit from lower transaction fees compared to traditional methods.

Blockchain technology offers quicker settlements and lower fees for simple funds transfers and peer-to-peer payments, although the exact fees may vary depending on the implementation and use case of the blockchain network.

3. No Single Point of Failure

Blockchain’s decentralized design boosts security by removing vulnerable single points.

Unlike centralized systems where a server breach can cause major problems, blockchain’s distributed ledger shares data across many nodes, ensuring it’s secure and cannot be tampered with.

Every node helps confirm information’s authenticity through agreement before it’s added to the ledger.

This greatly lowers the chance of unauthorized data changes or fraud, as it’s hard for anyone to add fake data or change records without agreement from the network.

Additionally, the agreement process and automation lessen the chance of mistakes, improving data accuracy.

In summary, blockchain’s decentralized structure and agreement method offer strong security, protecting against different risks and ensuring the network’s trustworthiness.

4. Censorship-resistant

Public blockchains offer censorship resistance, meaning they make it hard for powerful entities to shut down systems unfairly, which usually hurts regular people the most.

Unlike centralized systems, where one authority has control, blockchain spreads data across many nodes, making it tough for any one group to censor information.

The decentralized setup ensures data exists in many places, making it almost impossible to censor completely. New tech like sharding makes it even harder to shut down the whole blockchain.

As blockchain evolves, efforts to resist censorship grow, giving people more power over their data and transactions.

5. Improved Security and Privacy

Blockchain is more secure than centralized systems because it’s decentralized. Changes to records are easy to spot because copies are compared automatically, and there are digital signatures.

Also, users don’t have to share personal or financial info, which protects data from hackers.

Blockchain’s structure is tough and decentralized, so even if some nodes fail, the network keeps going.

Cryptography makes data security strong, making it hard for hackers to get in. Overall, blockchain’s secure and decentralized nature makes it a reliable way to store and manage data.

6. Transparent & Universal Recording System

Blockchain records transactions in a ledger anyone can see online. While wallet balances are visible, the owner’s identity stays private. Each wallet could belong to an individual or a group, balancing transparency with privacy.

Once data is in the ledger, it can’t be changed or deleted, thanks to cryptographic techniques.

Trying to change data creates a unique identifier, alerting others to tampering. The ledger is usually open for everyone to see, boosting transparency across the network.

Cons of Blockchain Technology

Now, let’s look at the downsides of blockchain technology.

1. Scalability

Scalability is a big challenge for blockchain. It struggles to handle lots of transactions quickly because each transaction needs approval from most nodes, slowing things down and making fees higher.

Also, it doesn’t always work smoothly with older systems that many businesses still use. Sometimes, switching to blockchain means getting rid of those old systems entirely, which can be tough and met with doubt or pushback.

In short, when thinking about using blockchain, it’s important to remember how tricky it can be to fit into existing setups.

2. No Control for Enterprises

Enterprises might not have as much control with blockchain compared to traditional systems. Public blockchains, in particular, might lack the level of authority some organizations need.

But there’s hope. Private and consortium blockchains, called enterprise blockchain frameworks, are coming up. They blend blockchain’s distributed nature with the control of traditional systems.

Keep in mind, though, that blockchain is open-source. That means it can be changed and used differently by different groups to fit their needs.

3. Uncertain Regulations

The lack of clear rules can be a big problem for using blockchain. This uncertainty also makes it easier for scams, like fake token sales, to happen.

Plus, without clear regulations, governments and big companies might not want to use blockchain. They’re cautious about systems that aren’t controlled like other financial tech.

4. Vulnerable to Hacking Attacks

Blockchain makes our records and assets safer, but it’s still new. And when we talk about blockchain, we’re not just talking about individual platforms like L1.

L1 blockchains, like Ethereum, boast robust security against breaches thus far. To simplify, L1 blockchains can be likened to operating systems in the Web2 realm, utilized by various applications to provide services to users.

However, ancillary solutions operating around L1 blockchains, like bridges for token swaps, often lack the same level of security afforded by consensus algorithms inherent in L1 blockchains.

Moreover, their insufficient decentralization renders them vulnerable to malicious activities on public networks.

Additionally, classic rug pulls, a form of scam where developers abandon a project and abscond with investors’ funds, are prevalent in both traditional finance and the Web3 industry.

Upon closer examination, these trends bear a striking resemblance to the internet’s early days in the late 1990s and early 2000s, characterized by reports of malware, phishing, and cybercrimes.

Essentially, any new system or protocol remains susceptible to exploitation by bad actors seeking to pilfer funds or cause harm.

5. Slower

The speed of blockchain technology is hindered by its lack of scalability, a significant drawback.

Blockchains are favored for their cost efficiency and quick settlement in simple peer-to-peer payments and cross-border fund transfers.

However, more complex transactions in areas such as supply chains and identity management can be slower than traditional technologies.

For instance, blockchain networks such as Bitcoin and Ethereum have limited processing capabilities, handling no more than 20 transactions per second (TPS), whereas counterparts in the Web2 realm like Visa and Nasdaq can manage up to 5000 TPS.

Industries like gaming, which entail millions of microtransactions per millisecond, require a high-throughput infrastructure.

The slower pace of blockchain transactions stems from the computational demands inherent in blockchain technology, which can be more repetitive compared to centralized servers.

Each time the ledger is updated, all or most nodes in the network must also update their copies, necessary due to the distributed ledger’s nature but contributing to transaction processing delays.

However, newer blockchain platforms like Ethereum are striving to achieve limitless scalability through innovative protocols.

6. Cultural Disruption

An inherent drawback of adopting blockchain technology is its potential to disrupt established business models and cultural norms.

This is because blockchain has the capability to fundamentally alter the operations of systems and industries, posing a challenge for organizations accustomed to traditional models to adapt to these changes.

In certain scenarios, the integration of blockchain technology may render certain marketplaces and industries obsolete, as it reshapes the dynamics of business operations and interactions.

It is imperative for organizations to meticulously assess the implications of blockchain on their business models and operations, weighing the advantages and disadvantages before determining its utilization.

What is Blockchain Technology?

Blockchain technology is a decentralized digital ledger system used for recording and verifying transactions across a network of computers.

It’s transparent, secure, and tamper-proof due to its decentralized structure and cryptographic techniques.

It’s best known for powering cryptocurrencies like Bitcoin but has various applications beyond finance, such as supply chain management and identity verification.

Conclusion

In this article, you will learn about the blockchain technology pros and cons. Blockchain technology offers benefits like decentralization and security but faces challenges such as scalability and regulatory uncertainty.

Despite limitations, its ongoing evolution promises transformative changes across industries. A balanced approach is crucial for maximizing its potential in the digital landscape.

F.A.Q

What is blockchain technology❓

Blockchain technology is a decentralized digital ledger system used for recording and verifying transactions across a network of computers. It ensures transparency, security, and tamper-proof data storage.

What are the main advantages of blockchain technology❓

The main advantages include decentralization, low cost, elimination of single points of failure, censorship resistance, security and confidentiality, and transparent recording of transactions.

What are the key drawbacks of blockchain technology❓

The main drawbacks include scalability issues, lack of control for enterprises, regulatory uncertainty, vulnerability to hacking attacks, slower transaction speeds compared to traditional methods, and potential cultural disruption.

How does blockchain increase security and confidentiality❓

Blockchain technology offers heightened security by decentralizing data storage, making it difficult for unauthorized parties to manipulate or access information. It also ensures confidentiality by not requiring users to disclose personal or financial details.

Can blockchain technology integrate with existing legacy systems❓

While blockchain technology can integrate with existing systems, it may pose challenges, especially in terms of scalability and compatibility. In some cases, the adoption of blockchain may require significant modifications or complete replacement of legacy networks.